THE EXPECTED IMPACT OF THE CRISIS ON THE OIL

MARKET CONDITIONS

Crude oil prices reached a record high of US$ 147 per barrel (US$/b) in July 2008 on the back of a six-year commodity boom cycle driven mostly by demand from developing countries.1 However, as of August 2008, oil prices plunged rapidly as demand from the Organisation for Economic Co-operation and Development (OECD) countries came to a sudden halt and recession loomed as the financial crisis severely

impacted the global economy (IDS, 2008, p. 5). In an attempt to curb falling prices, the Organization of Petroleum Exporting Countries (OPEC) introduced a series of cuts in output. At the time of writing, oil prices have begun to stabilize at levels ranging in the mid US$ 40 per barrel

OIL DEMAND

According to the EIU, world oil demand is falling. It is estimated that demand fell by 0.2 per cent in 2008 and expected to fall by 0.4 per cent in 2009. Plummeting world demand is largely driven by falling consumption in developed countries. Indeed, preliminary estimates point to a decline of 2.9 per cent in oil

demand in OECD countries in 2008. A further drop of 1.8 per cent is also forecast in 2009. Reduction in demand in OECD countries is largely due to falling demand in North America, estimated at about 2 per cent in 2009, and in Europe, estimated at 1.7 per cent.

Non-OECD demand for oil is forecast to grow by 1.4 per cent in 2009 and by 2.3 per cent in 2010.Underpinning these estimates is the expected increase in demand in developing countries. However, even if that demand is expected to increase, it will not be sheltered from the consequences of the global economic turmoil, as it is forecast to grow at a slower pace over the short-to-medium term. Broadly speaking, growing oil demand in developing countries has recently been driven by two major components, namely increasing demand in both China and India and Arab oil-exporting countries. Hence, the extent to which oil demand in developing countries will be impacted largely depends on the underlying elements in each of the abovementioned components. The expected slowdown in the demand for oil in emerging countries is greatly dependent on the demand outlook in China and India which is, in turn, related to their growth prospects.According to the EIU, Chinese oil consumption will grow by just 2.5 per cent in 2009 (down from a 4.8 per cent growth the previous year), and by 3.5 per cent in 2010.

Thursday, March 18, 2010

‘Pakistan’s oil reserves will last only 6 days’

Islamabad, Jan 26 (IANS) Pakistan’s petroleum reserves will last only six days and its furnace oil stock will run out in nine days, a media report said Monday.Confirming this, Petroleum Ministry Additional Secretary G.A. Sabri told GEO TV: “We are currently importing petroleum products based on 10 days’ inventory keeping in view the dollar constraints.”

According to data available with GEO TV, in the corresponding period of the last year, the country had petrol reserves for 20 days and furnace oil for 21 days.

Pakistan annually requires some 60 million tonnes of oil, two-thirds of which is imported. Oil meets about 43.5 percent of the nation’s primary energy needs, natural gas 38.3 percent and coal 5.1 percent, while the remainder is met by hydro-electricity and nuclear power.

More at : ‘Pakistan’s oil reserves will last only 6 days’

Islamabad, Jan 26 (IANS) Pakistan’s petroleum reserves will last only six days and its furnace oil stock will run out in nine days, a media report said Monday.Confirming this, Petroleum Ministry Additional Secretary G.A. Sabri told GEO TV: “We are currently importing petroleum products based on 10 days’ inventory keeping in view the dollar constraints.”

According to data available with GEO TV, in the corresponding period of the last year, the country had petrol reserves for 20 days and furnace oil for 21 days.

Pakistan annually requires some 60 million tonnes of oil, two-thirds of which is imported. Oil meets about 43.5 percent of the nation’s primary energy needs, natural gas 38.3 percent and coal 5.1 percent, while the remainder is met by hydro-electricity and nuclear power.

More at : ‘Pakistan’s oil reserves will last only 6 days’

Wednesday, March 17, 2010

oil consumption per day

This entry is the total oil consumed in barrels per day (bbl/day). The discrepancy between the amount of oil produced and/or imported and the amount consumed and/or exported is due to the omission of stock changes, refinery gains, and other complicating factors.

See also: Oil - consumption bar chart

Country Name Value

United States 20,800,000

China 6,930,000

Japan 5,353,000

Russia 2,916,000

Russia 2,916,000

Germany 2,618,000

India 2,438,000

Canada 2,290,000

Korea, South 2,130,000

Brazil 2,100,000

Mexico 2,078,000

Saudi Arabia 2,000,000

France 1,999,000

United Kingdom 1,820,000

Italy 1,732,000

Iran 1,630,000

Spain 1,600,000

Indonesia 1,100,000

Netherlands 1,011,000

Thailand 929,000

Australia 903,200

Taiwan 816,700

Singapore 802,000

Turkey 660,800

Egypt 635,000

Venezuela 599,000

Belgium 591,000

South Africa 519,000

Malaysia 501,000

Argentina 480,000

Poland 462,700

Greece 415,700

United Arab Emirates 372,000

Sweden 363,200

Pakistan 345,000

Philippines 340,000

Kuwait 333,000

Portugal 305,800

Nigeria 302,000

Austria 295,100

Iraq 295,000

Hong Kong 292,000

This entry is the total oil consumed in barrels per day (bbl/day). The discrepancy between the amount of oil produced and/or imported and the amount consumed and/or exported is due to the omission of stock changes, refinery gains, and other complicating factors.

See also: Oil - consumption bar chart

Country Name Value

United States 20,800,000

China 6,930,000

Japan 5,353,000

Russia 2,916,000

Russia 2,916,000

Germany 2,618,000

India 2,438,000

Canada 2,290,000

Korea, South 2,130,000

Brazil 2,100,000

Mexico 2,078,000

Saudi Arabia 2,000,000

France 1,999,000

United Kingdom 1,820,000

Italy 1,732,000

Iran 1,630,000

Spain 1,600,000

Indonesia 1,100,000

Netherlands 1,011,000

Thailand 929,000

Australia 903,200

Taiwan 816,700

Singapore 802,000

Turkey 660,800

Egypt 635,000

Venezuela 599,000

Belgium 591,000

South Africa 519,000

Malaysia 501,000

Argentina 480,000

Poland 462,700

Greece 415,700

United Arab Emirates 372,000

Sweden 363,200

Pakistan 345,000

Philippines 340,000

Kuwait 333,000

Portugal 305,800

Nigeria 302,000

Austria 295,100

Iraq 295,000

Hong Kong 292,000

oil problem in pakistan

The problem with Pakistan is that we have not explored our land and off Shore assets properly and resource developement activities are Nil because of Unstable Economy. Major Players in Oil only come forward when Exploration Studies are conducted in a allocated area by GOP. Pakistan has a vast Potential of Oil and to date 833 Million Barrels of Oil reserve are there. But it is only 5% of the exploration conducted on the In and OFF Shore areas.

Oil Exploration is not a child's Play but requires a open resource developement and Energy policy to make Private Companies and Investors to take interest and requires consistency in policy which pakistan lacks since it came into being.

Pakistan contains two sedimentary basins: Indus in the east and Balochistan in the west.The Indus basin has received sediments from precambrian until Recent, albeit with breaks.It has been producing hydrocarbons since 1914 from three main producing regions, namely, the Potwar, Sulaisman, and Kirthar.In the Potwar, oil has been discovered in Cambrian, Permian, Jurassic, and Tertiary rocks.Potential source rocks are identified in Infra-Cambrian, Permian, Paleocene, and Eocene successions, but Paleocene/Eocene Patala Formation seems to be the main source of most of the oil.In the Sulaiman, gas has been found in Cretaceous and Tertiary; condensate in Cretaceous rocks.Potential source rocks are indicated in Cretaceous, Paleocene, and Eocene successions.The Sembar Formation of Early Cretaceous age appears to be the source of gas.In the Kirthar, oil and gas have been discovered in Cretaceous and gas has been discovered in paleocene and Eocene rocks.Potential source rocks are identified in Kirthar and Ghazij formations of Eocene age in the western part.However, oil- and gas-producing Badin platform area, has recognized the Sembar Formation of Early Cretaceous age as the only source of Cretaceous oil and gas.The Balochistan basin is part of an Early Tertiary arc-trench system.The basin is inadequately explored, and there is no oil or gas discovery so far.However, potential source rocks have been identified in Eocene, Oligocene, Miocene, and Pliocene successions based on geochemical analysis of surface samples.Mud volcanoes are present.

The problem with Pakistan is that we have not explored our land and off Shore assets properly and resource developement activities are Nil because of Unstable Economy. Major Players in Oil only come forward when Exploration Studies are conducted in a allocated area by GOP. Pakistan has a vast Potential of Oil and to date 833 Million Barrels of Oil reserve are there. But it is only 5% of the exploration conducted on the In and OFF Shore areas.

Oil Exploration is not a child's Play but requires a open resource developement and Energy policy to make Private Companies and Investors to take interest and requires consistency in policy which pakistan lacks since it came into being.

Pakistan contains two sedimentary basins: Indus in the east and Balochistan in the west.The Indus basin has received sediments from precambrian until Recent, albeit with breaks.It has been producing hydrocarbons since 1914 from three main producing regions, namely, the Potwar, Sulaisman, and Kirthar.In the Potwar, oil has been discovered in Cambrian, Permian, Jurassic, and Tertiary rocks.Potential source rocks are identified in Infra-Cambrian, Permian, Paleocene, and Eocene successions, but Paleocene/Eocene Patala Formation seems to be the main source of most of the oil.In the Sulaiman, gas has been found in Cretaceous and Tertiary; condensate in Cretaceous rocks.Potential source rocks are indicated in Cretaceous, Paleocene, and Eocene successions.The Sembar Formation of Early Cretaceous age appears to be the source of gas.In the Kirthar, oil and gas have been discovered in Cretaceous and gas has been discovered in paleocene and Eocene rocks.Potential source rocks are identified in Kirthar and Ghazij formations of Eocene age in the western part.However, oil- and gas-producing Badin platform area, has recognized the Sembar Formation of Early Cretaceous age as the only source of Cretaceous oil and gas.The Balochistan basin is part of an Early Tertiary arc-trench system.The basin is inadequately explored, and there is no oil or gas discovery so far.However, potential source rocks have been identified in Eocene, Oligocene, Miocene, and Pliocene successions based on geochemical analysis of surface samples.Mud volcanoes are present.

Tuesday, March 16, 2010

pakistan oil crisis

ISLAMABAD, Dec 10: Pakistan’s oil reserves have plummeted to the lowest-ever level in the country’s history and the stocks of major oil products — kerosene and diesel — are sufficient for six days only.

Under the standard operating procedures (SOPs), the government and its companies are required to maintain a minimum of 21-day stocks of every product at all times to cope with any eventuality. The SOPs are defined in the ‘Blue Book’ meant for strategic government organisations to handle crises.

Informed sources told Dawn that the situation had not aggravated in a day or two. The ministry of petroleum had been informing the government about the situation consistently since late October.

Despite repeated attempts, Petroleum Secretary Farrukh Qayyum and additional secretary Shaukat Hayat Durrani could not be reached for comment.

However, according to petroleum experts, there will be no immediate impact of the depletion on the common man. But the situation can lead to a crisis in future and should be handled with extreme care, they added. Statistics confirmed by sources in the petroleum ministry and oil industry reveal that total kerosene stocks at present stood at less than 3,800 tons, sufficient only for four days.

Pakistan’s current kerosene requirement is 920 tons per day. The country has total kerosene storage capacity for 80 days and the current storage is about nine per cent of the total capacity.

Likewise, current high speed diesel stocks are at around 125,457 tons, which can meet consumption requirement of six days at the average need of about 22,000 tons per day. The country has the capacity to store HSD to the extent of 39 days of requirement. As such, total usable stocks are about 19 per cent of the available capacity.

Light diesel oil, comparatively a low-consumption product, has a stock of about 2,500 tons that is enough for four days, at the rate of 558 tons per day, which is 14 per cent of its total storage capacity of about 42 days of consumption.

The situation is comparatively better for furnace oil, petrol, HOBC and jet fuel as their stocks were enough for 26 days, 15 days, 22 days and 20 days, respectively, are much lower than last year.

The country has storage capacity of these products for 75 days, 33 days, 131 days and 34 days, respectively. This means that only 39 per cent, 49 per cent, 21 per cent and 49 per cent of storage capacity is being utilised at the moment.

The sources said the major reason for the drop in stocks was cash problems faced by the oil companies to have sufficient imports and non-availability of cargo in Arab countries because of advance supply orders.

Secondly, some of the refineries have increased their jet fuel production that directly affects kerosene production because both are alternative products.

The punchline, however, is that kerosene is a subsidised product that affects oil companies’ cash flow in the wake of price differential claim while jet fuel is a cash product and attracts payments in dollars it is sold to allied forces engaged in the “war on terror”.

With no real increase in domestic consumption, Pakistan’s oil import bill was estimated at $8.8 billion when the budget was announced, but this figure was likely to exceed $10 billion, the sources said.

The government had estimated that crude price would not exceed 70 dollars per barrel, but it went up as high as 98 dollars per barrel.

Diesel is usually described as ‘killer fuel’ because of its harmful impact on the environment. About 7.5 million tons of diesel was consumed in the country, as against a total oil consumption of 17.5 million tons. Furnace oil has the second largest share and remains in the range of 5-7 million tons depending upon power production requirements.

ISLAMABAD, Dec 10: Pakistan’s oil reserves have plummeted to the lowest-ever level in the country’s history and the stocks of major oil products — kerosene and diesel — are sufficient for six days only.

Under the standard operating procedures (SOPs), the government and its companies are required to maintain a minimum of 21-day stocks of every product at all times to cope with any eventuality. The SOPs are defined in the ‘Blue Book’ meant for strategic government organisations to handle crises.

Informed sources told Dawn that the situation had not aggravated in a day or two. The ministry of petroleum had been informing the government about the situation consistently since late October.

Despite repeated attempts, Petroleum Secretary Farrukh Qayyum and additional secretary Shaukat Hayat Durrani could not be reached for comment.

However, according to petroleum experts, there will be no immediate impact of the depletion on the common man. But the situation can lead to a crisis in future and should be handled with extreme care, they added. Statistics confirmed by sources in the petroleum ministry and oil industry reveal that total kerosene stocks at present stood at less than 3,800 tons, sufficient only for four days.

Pakistan’s current kerosene requirement is 920 tons per day. The country has total kerosene storage capacity for 80 days and the current storage is about nine per cent of the total capacity.

Likewise, current high speed diesel stocks are at around 125,457 tons, which can meet consumption requirement of six days at the average need of about 22,000 tons per day. The country has the capacity to store HSD to the extent of 39 days of requirement. As such, total usable stocks are about 19 per cent of the available capacity.

Light diesel oil, comparatively a low-consumption product, has a stock of about 2,500 tons that is enough for four days, at the rate of 558 tons per day, which is 14 per cent of its total storage capacity of about 42 days of consumption.

The situation is comparatively better for furnace oil, petrol, HOBC and jet fuel as their stocks were enough for 26 days, 15 days, 22 days and 20 days, respectively, are much lower than last year.

The country has storage capacity of these products for 75 days, 33 days, 131 days and 34 days, respectively. This means that only 39 per cent, 49 per cent, 21 per cent and 49 per cent of storage capacity is being utilised at the moment.

The sources said the major reason for the drop in stocks was cash problems faced by the oil companies to have sufficient imports and non-availability of cargo in Arab countries because of advance supply orders.

Secondly, some of the refineries have increased their jet fuel production that directly affects kerosene production because both are alternative products.

The punchline, however, is that kerosene is a subsidised product that affects oil companies’ cash flow in the wake of price differential claim while jet fuel is a cash product and attracts payments in dollars it is sold to allied forces engaged in the “war on terror”.

With no real increase in domestic consumption, Pakistan’s oil import bill was estimated at $8.8 billion when the budget was announced, but this figure was likely to exceed $10 billion, the sources said.

The government had estimated that crude price would not exceed 70 dollars per barrel, but it went up as high as 98 dollars per barrel.

Diesel is usually described as ‘killer fuel’ because of its harmful impact on the environment. About 7.5 million tons of diesel was consumed in the country, as against a total oil consumption of 17.5 million tons. Furnace oil has the second largest share and remains in the range of 5-7 million tons depending upon power production requirements.

Monday, March 15, 2010

'Peak Oil Crisis'

It is a Peak Oil news and resource site for those interested in the issue of Peak Oil. We are UK based but are interested in stories from anywhere this global problem manifests itself.

For those of you who haven't come across this phrase before, the term Peak Oil is used to describe the global maximum in conventional crude oil production which is predicted to happen in the not too distant future (if it hasn't happened already). The concept was devised by geologist Marion King Hubbert who worked for oil company Shell and who correctly predicted that in 1970 the crude oil production within the United States would peak and then decline. He then went on to say that the same thing would happen to world crude oil production eventually.

Once this maximum (or peak) has been reached global oil production will generally decline forever afterwards. It is something that will only become apparent some time after the event has happened due to fluctuations in oil production from year to year.

At the moment it appears that oil production is on a plateau with a peak occurring sometime in 2006. Production is struggling to stand still let alone increase. It is thought that global oil production from mature oil fields is declining at a rate of between 6-7% per year. This means that at current oil demand, around another 5 million barrels of new oil (crude & other liquid fuels) per day must come on line per year. This is just about happening at the moment but is getting harder everyday at oil becomes more difficult, expensive and energy intensive to extract. Also as a result of the current world economic problems and lower prices oil exploration activity has been curtailed significantly.

Peak Oil is thought to occur when roughly half of the world's oil reserves have been used up. All oil fields peak and then decline by their very nature and the concept of global Peak Oil is simply the extrapolation of this idea to the sum of all known oil fields. Peak Oil is thought to be imminent because there have been fewer 'super giant' oil field discoveries in recent years to put any potential peak in production further into the future.

It is a Peak Oil news and resource site for those interested in the issue of Peak Oil. We are UK based but are interested in stories from anywhere this global problem manifests itself.

For those of you who haven't come across this phrase before, the term Peak Oil is used to describe the global maximum in conventional crude oil production which is predicted to happen in the not too distant future (if it hasn't happened already). The concept was devised by geologist Marion King Hubbert who worked for oil company Shell and who correctly predicted that in 1970 the crude oil production within the United States would peak and then decline. He then went on to say that the same thing would happen to world crude oil production eventually.

Once this maximum (or peak) has been reached global oil production will generally decline forever afterwards. It is something that will only become apparent some time after the event has happened due to fluctuations in oil production from year to year.

At the moment it appears that oil production is on a plateau with a peak occurring sometime in 2006. Production is struggling to stand still let alone increase. It is thought that global oil production from mature oil fields is declining at a rate of between 6-7% per year. This means that at current oil demand, around another 5 million barrels of new oil (crude & other liquid fuels) per day must come on line per year. This is just about happening at the moment but is getting harder everyday at oil becomes more difficult, expensive and energy intensive to extract. Also as a result of the current world economic problems and lower prices oil exploration activity has been curtailed significantly.

Peak Oil is thought to occur when roughly half of the world's oil reserves have been used up. All oil fields peak and then decline by their very nature and the concept of global Peak Oil is simply the extrapolation of this idea to the sum of all known oil fields. Peak Oil is thought to be imminent because there have been fewer 'super giant' oil field discoveries in recent years to put any potential peak in production further into the future.

Sunday, March 7, 2010

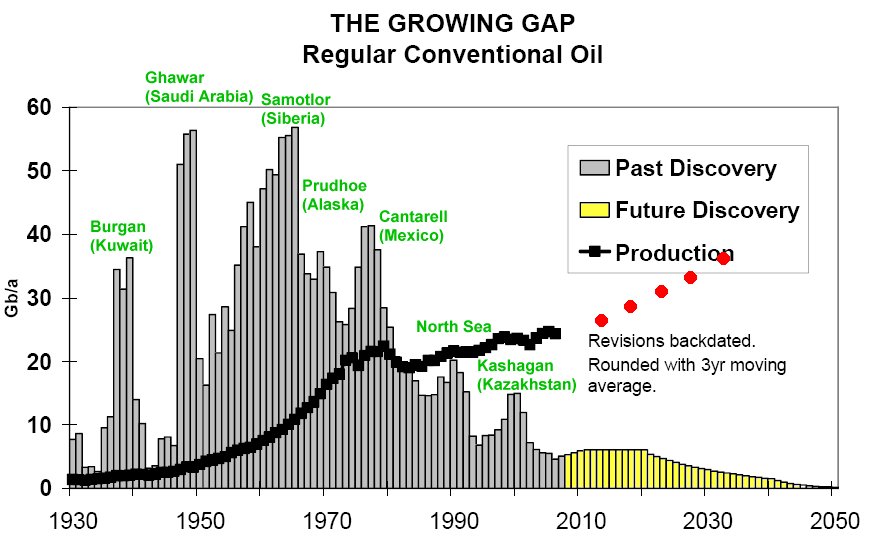

The Growing gap

- This graphic is worth careful study.It shows oil discoveries and oil consumption since 1930 to 2008. The black line shows oil consumption. Notice the peak in consumption in 1979 corresponding to the first oil crisis. The subsequent 5 year decline in oil consumption is attributed to more fuel efficient transportation and a slowing world economy. The grey bars show oil discoveries. Notable grey bar features include Kuwait's big oil field, Burgan, which was discovered in the late 30s and Ghawar, the world's largest oil field, which was discovered in 1948. Note that the discovery rate peaked around 1966. Note also that consumption exceeds discoveries every year since 1984. Now there is a large gap between discoveries and production. None of this is controversial--it is only history.

- What happens after 2008 is extrapolation and speculation. The EIA (Energy Information Agency) has projected a 1.6% annual growth in oil demand which is shown in red. Developed countries, for example the USA, Germany and Japan are not expected to increase consumption. In fact, consumption might decrease because of efficiency gains. But China and India both have booming economies. Automobile ownership increased by 37% in China and 17% in India in 2007.

- The yellow bars represent a guess about yet-to-find oil. The yellow bars show no declines in the discovery rate until 2021. That seems optimistic given the declining discovery rate in the previous decade.

- Note the growing gap between discoveries and production!

The Conclusion

- Oil discovered 40 years ago is the basis of current oil production. The search for oil continues but projected oil discoveries will contribute little to projected oil production in 2030. The declining rate of oil discoveries makes it painfully obvious--most of the oil has already been discovered. The technology for finding oil has improved greatly since the major discoveries, yet little oil has been found in recent years. THe heyday of oil discovery was from 1950 to 1980. It is difficult to avoid the conclusion--most of the oil has been found.

- There is a growing gap between discoveries and production.

- World oil production is running flat out. Only the Saudis claim to have the ability to produce more though some dispute this. It is not a simple matter of turning a spigot or pumping faster. Oil fields can be permanently damaged by attempting to produce too fast.

- Soon there will be a gap between production and demand.

It Gets Worse

- According to BP (British Petroleum) world oil reserves stand at 1238 billion barrels. At present (2008) yearly world oil production stands at 31 billion barrels. There is enough oil to last 40 years if production holds constant and no new oil is found. According to BP, the Middle East has 61% of the world's oil reserves. Africa has 9.6% and the Russian Federation has 6.4%. The two countries sharing borders with the United States, Mexico and Canada, together have only 3.2%. Venezeula, a short distance away via oil tanker, has 7%

- The United States possesses 2.6% of the worlds oil reserves while it consumes 24% of the world's oil production.

- Although the United States has only 2.4% of the world's oil, it produces 9.2%. If the production rate could be maintained, the oil will be gone in 11 years. The figures for Canada are the same and they are worse for Mexico. The Middle East has enough oil to last 88 years at present production rates. Africa has 33 years. Clearly the United States will be increasingly dependent on oil imported from those places. It is impossible to consider oil independence in light of these numbers.

- The majority of the world's oil comes from old oil fields. For example, Kuwait still supplies 3% of the world's oil from a 70 year old field. The world's largest oil field, Ghawar, a 57 year old oil field, still supplies 5% of the world's oil. The North Sea (discovered in 1963) was exploited very quickly and is now in steep decline. Alaska's Prudhoe Bay (discovered in 1968) is now a trickle.

- Oil varies greatly in quality. Some oil is so light and sweet (low in sulfur) it can be pumped directly into the fuel tank of a Diesel truck. Some oil is more like tar and it may contain sulfur. It's hard to transport and natural gas may be needed to refine it into useful fuel. The oil from Manifa, a large oil field in Iran, is an extreme example. It contains so much sulfur and vanadium it can't be refined using today's technology. The average quality of oil is declining because the best quality was produced first.

- Oil varies greatly in accessibility. It is convenient to access Kuwaiti oil. Oil tankers in the Persian Gulf load from nearby Kuwaiti oil wells. It is inconvenient to access oil from the north slope of Alaska. It was necessary to build an 800 mile pipeline over mountains and permafrost to reach the oil in Prudhoe Bay. Oil drilling platforms can reach oil in mile deep water but only at great expense in money terms and in energy terms. There is oil in the arctic but oil drilling platforms will have to deal with ice and deep water to access it.

- The remaining oil will be expensive and difficult to produce, refine and transport.

Tuesday, February 23, 2010

The 1970s Energy Crisis was a period in which the major industrial nations of the world, particularly the United States, faced substantial shortages, both perceived and real, of petroleum. The two worst crises of this period were the 1973 oil crisis, caused by the Arab Oil Embargo of OAPEC, and the 1979 energy crisis, caused by the Iranian Revolution.

The crisis period, however, was triggered by events at the end of the 1960s. It was during this time that petroleum production in the United States and some other parts of the world peaked. Subsequently during the 1970s world oil production per capita peaked.

The major industrial centers of the world were forced to contend with escalating issues related to petroleum supply. The fact that Western nations had to deal with potentially unfriendly sources in the Middle East and other parts of the world to maintain supply made the situation especially complex.

The crisis led to stagnant economic growth in some nations, particularly the U.S., as oil prices climbed. Though there were genuine issues with supply, part of the run-up in prices resulted from the perception of a crisis. The combination of stagnant growth and price inflation during this era led to the coinage of the term stagflation.

By the 1980s both the recessions of the 1970s and adjustments in local economies to become more efficient in petroleum usage had controlled demand sufficiently that petroleum prices worldwide began to return to more sustainable levels.

The period was not uniformly negative for all economies. Petroleum-rich nations in the Middle East benefitted tremendously from increased prices and the slowing production in other areas of the world. Some other nations, such as Norway, Mexico, and Venezuela, benefitted as well. In the United States, the states of Texas and Alaska, as well as some other oil-producing areas, experienced major economic booms due to soaring oil prices even as most of the rest of the nation struggled with the stagnant economy. Many of these economic gains, however, came to a halt as prices stabilized and dropped in the 1980s.

The crisis period, however, was triggered by events at the end of the 1960s. It was during this time that petroleum production in the United States and some other parts of the world peaked. Subsequently during the 1970s world oil production per capita peaked.

The major industrial centers of the world were forced to contend with escalating issues related to petroleum supply. The fact that Western nations had to deal with potentially unfriendly sources in the Middle East and other parts of the world to maintain supply made the situation especially complex.

The crisis led to stagnant economic growth in some nations, particularly the U.S., as oil prices climbed. Though there were genuine issues with supply, part of the run-up in prices resulted from the perception of a crisis. The combination of stagnant growth and price inflation during this era led to the coinage of the term stagflation.

By the 1980s both the recessions of the 1970s and adjustments in local economies to become more efficient in petroleum usage had controlled demand sufficiently that petroleum prices worldwide began to return to more sustainable levels.

The period was not uniformly negative for all economies. Petroleum-rich nations in the Middle East benefitted tremendously from increased prices and the slowing production in other areas of the world. Some other nations, such as Norway, Mexico, and Venezuela, benefitted as well. In the United States, the states of Texas and Alaska, as well as some other oil-producing areas, experienced major economic booms due to soaring oil prices even as most of the rest of the nation struggled with the stagnant economy. Many of these economic gains, however, came to a halt as prices stabilized and dropped in the 1980s.

Subscribe to:

Posts (Atom)